What is the Potential of Indonesia

Healthcare Market?

Indonesia

Healthcare Market has shown a

positive incline during 2012-2017 but with respect to the expanding population

of Indonesia, the market is still underserved especially in the underdeveloped

and rural areas as of 2017. People across Indonesia are facing several health

care issues due to sedentary lifestyle and fast food consumption habits, such

as obesity, diabetes, and other cardiovascular diseases, which are demanding

for technologically advanced healthcare infrastructure. The healthcare market

has increased on the account of increasing healthcare facilities, innovation in

pharmaceutical manufacturers and clinical laboratory services and expansion of

pharmacy retail chains across the country. The market has witnessed innovation

in nutritional health segment, biopharmaceuticals and specialty pharmaceutical

products.

Hospitals

in the country contributed to the maximum share of overall healthcare market as

of 2016. Over ~% of the market revenues were generated from the hospitals

segment followed by the pharmaceutical market with ~% in 2017.

Indonesia

Healthcare market revenue has increased from USD ~ billion in 2012 to USD ~

billion in 2017 primarily due to rising prevalence of non-communicable and

lifestyle diseases including diabetes, asthma and heart disorders. The industry

has undergone various deregulation programs which has encouraged foreign

investment in the industry. Furthermore, increase in demand for generic

medicines has led the major players in the industry to expand their production

capabilities.

How Has the JKN Scheme Impacted the

Indonesia Pharmaceutical Market?

The

market size of Indonesia pharmaceutical industry has increased from USD ~

million in 2012 to USD ~ million in 2017 at a CAGR of ~%. The market is in the

growing stage supported by favorable government regulations and entry of

foreign players in the space.

During

2017, the domestic players dominate the market with major focus on production

of generic drugs. This is driven by the implementation of universal healthcare

system. The program has led to an increased demand for generic medicines from

public and private hospitals participating in the program.

Further,

the industry witnessed various deregulation programs which encouraged foreign

investment in the industry. For instance, the government removed the

pharmaceutical industry from its negative investment list implying 100% foreign

ownership is allowed. Major therapeutic segments was anti-infective due to the

prevalence of communicable diseases such as TB, influenza and others followed

by Gastrointestinal, cardiovascular, Central nervous system, respiratory,

musculoskeletal and dermatology.

How Have the Various Segments Performed

in Indonesia Pharmaceutical Market?

Anti-infective

drug sale has contributed to the largest share of ~% in the revenue share of

Indonesia Pharmaceutical industry in 2017. This is mainly due to high

prevalence of bacterial and communicable diseases. This segment is dominated by

prescription drugs since the patients infected with bacterial and viral

diseases need to consult a doctor for proper treatment of the particular

disease. This is followed by Gastrointestinal and metabolism drugs with ~%, cardiovascular

system drugs with ~%, Central Nervous system drugs with ~%, Respiratory system

drugs with ~%, Musculoskeletal system drugs with ~%, dermatology drugs with ~%,

genitourinary and hormonal drugs with ~%, blood related drugs with ~%, oncology

with ~% and rest of the therapeutic segments with ~% of the revenue share in

2017.

Domestic

players have accounted for ~% of the revenue in Indonesia pharmaceutical market

in 2017 driven by the implementation of JKN (National Health Insurance System)

in 2014. The product portfolio of majority domestic pharmaceutical companies is

dominated by generic drugs. International players have captured ~% of the

revenue share in 2017 driven by favorable government norms for foreign

ownership.

How Major Segments in Indonesia

Pharmaceutical Market have performed?

Generic

drugs have accounted for the major revenue share of ~% in 2017 driven by the

increased demand from government run hospitals and clinics. The share of

patented drugs has increased from ~% in 2013 to ~% in 2017. Further, ethical

generic drugs have accounted for ~% of the Indonesia generic drug market

revenue in 2017 followed by free sale drugs with ~% and unbranded drug sale

with ~%. The Prescription drugs sales have accounted for ~% of the revenue

share in Indonesia Pharmaceuticals Market. OTC drugs have accounted for ~% of

the revenue share in 2017 as more number of people took to self medication.

Domestic sales have accounted for a majority revenue share of ~% in 2017

whereas exports have accounted for a small share of ~%. The domestic market is

dominated by the sale of low priced ethical generic medicines. West java has

accounted for ~% of the pharmaceutical companies in 2016. This is followed by

Jakarta with ~%, East java with ~%, Central Java with ~% and others with ~% of

the companies

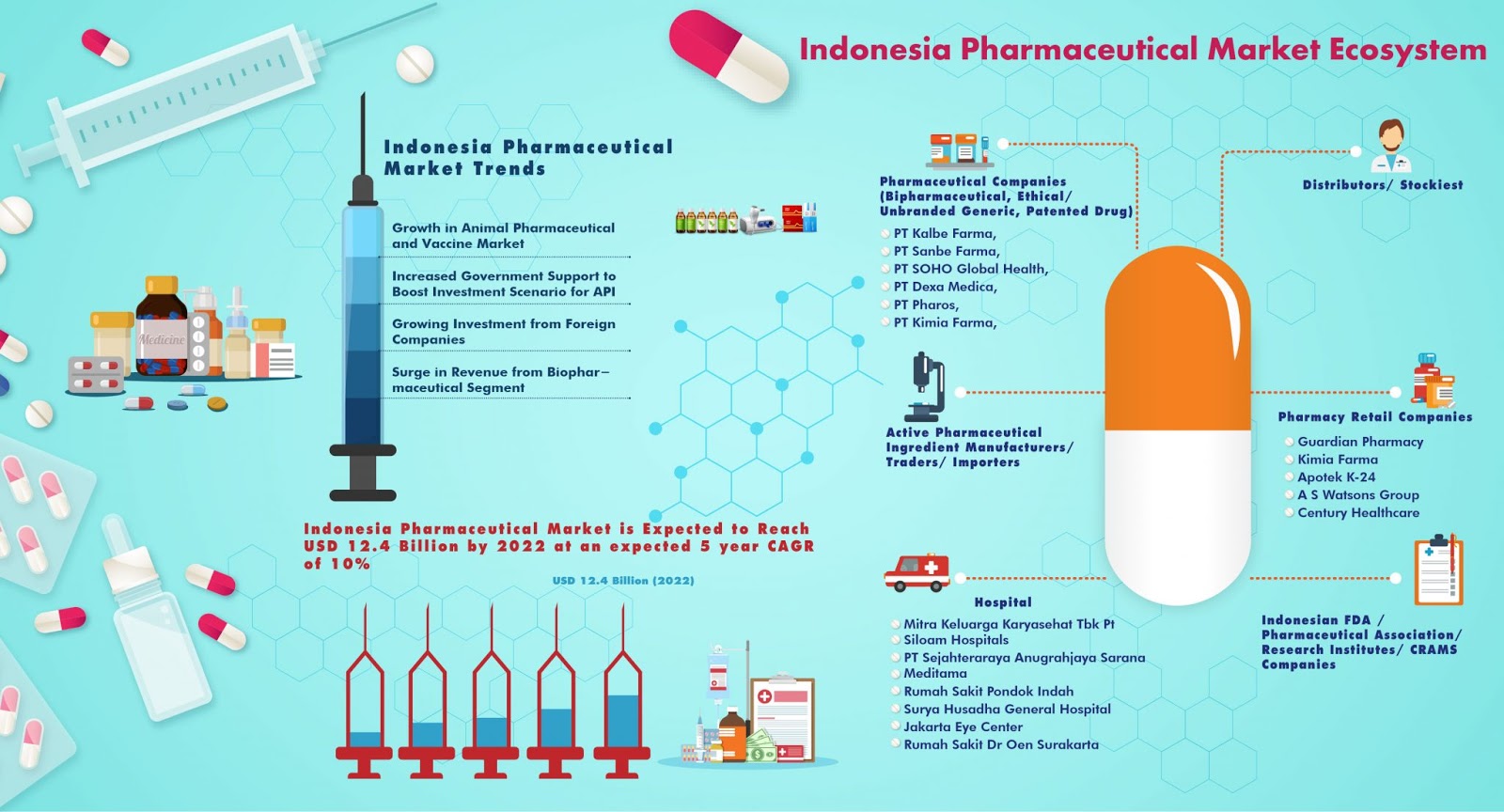

What are the major Trends and growth

Drivers in Indonesia Pharmaceutical Market?

Growth

in animal pharmaceutical has added to the overall market revenue. The animal

pharmaceuticals industry has benefitted from opportunities in terms of new

legislations for animal pharmaceuticals. With the launch of 11th economic

package, the government has aimed to boost the domestic production of

medicines' raw materials. Moreover, the government has removed the

pharmaceutical industry from its negative investment list (which lists the

sectors that are closed, or partially closed, for foreign ownership) implying

100% foreign ownership is allowed. The policy also encourages joint ventures

between foreign pharmaceutical companies and local ones in order to transfer

knowledge and technology. In addition to this, the government is planning to

offer fiscal incentives and making the investment procedure easier to attract

foreign players in the industry.

The

Universal healthcare system launched by the government in 2014 has led to an

increase in the production of generic medicines. This has led to lowering

margins as people have shifted from ethical drugs to prescribed generic drugs

but at the same time the sales volume has increased. The market has witnessed

rising number of mergers and acquisitions as a part of expansion strategy by

major domestic and international players.

How is the Competitive Ladscape of

Indonesia Pharmaceutical Market?

There

are ~ pharmaceutical companies (~ domestic and~ international companies)

located in Indonesia and ~% of them are located in Java in 2016. These players

compete on the basis of distribution network, product portfolio, marketing

activities and research and development. The domestic players dominate the

generic drug and OTC drug segment. The domestic players dominate the generic

drug and over the counter drug segment. International players have better

expertise, skilled labor and infrastructure to produce such medicines at

competitive prices.

What is the Future Potential of Indonesia

Pharmaceutical Market?

The

Indonesia pharmaceutical industry is expected to increase from USD ~ billion in

2018 to USD ~ billion at a growth rate of ~%. The industry growth will be led

by Indonesia’s large population and growing middle-income class, supportive

government policies and higher investment in the industry. With the increase in

incidence of communicable diseases such as HIV, TB, therapeutic segments such

as anti infectives and respiratory are expected to grow. Major companies are

expected to increase investment in nutritional and herbal medicines due to

changing preference in the industry. Apart from manufacturing generic and

patented drugs, pharmaceutical companies will shift focus to other niche

segments such as combined dosages, novel drug delivery areas. Further in order

to overcome the shortcomings, Contract Development and Manufacturing

Organizations (CDMOs) will emerge as an attractive resource for manufacturers

seeking to expand their capacities

For more information on the research

report, refer to below link:

Related Reports by Ken Research

https://www.kenresearch.com/healthcare/general-healthcare/uae-healthcare-market-report/37505-91.html

Contact:

Ken

Research

Ankur

Gupta, Head Marketing & Communications

+91-124-4230204