Indian pigment manufacturers are expanding their production capacities, given their low cost advantage with increasing focus on HPP and other specialized pigments such as metallic and pearlescent, used in automotives and other industrial coatings.

Pigment manufacturers in India, especially the organized sector players have started to focus on backward integration to gain a competitive advantage over others.

The growing trend of using aluminum based pigments in India has promoted the development of superior quality coating solutions, intense colors and new metallic shades which are further expected to boost the demand for metallic pigments in automotive and construction sector.

Surging pigment end-user expectations in terms of price and quality consciousness has forced manufacturers operating within the organized sector to invest more on R&D in order to develop both organic as well inorganic pigment emulsions within the regulatory framework and reasonable pricing in the coming years. Additionally, they have been opting for backward integration model therefore, procuring raw material in advance and producing in accordance with customer needs. As a result, it will also help them to reduce their overall cost of manufacturing.

Increasing consumer preference towards aesthetic finishes in passenger cars coupled with growth in the country’s automobile industry is further estimated to generate additional demand for metallic and pearlescent effect pigments towards paints and coating applications in India. Small and niche players can focus towards this product type owing to growing trend of adopting high performance organic pigments and the continuous displacement of heavy toxic metal pigments such as lead, chromium and others.

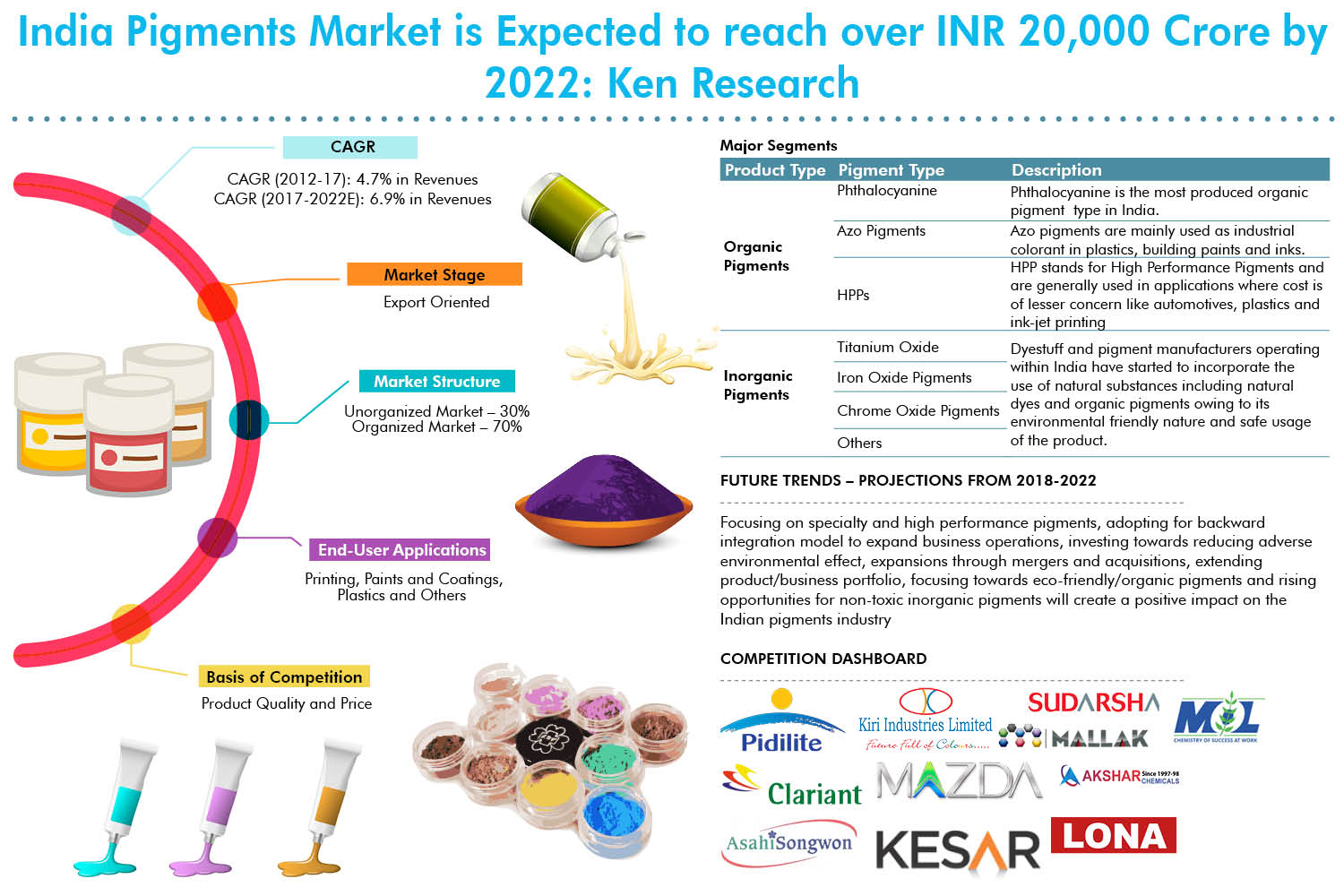

Analysts at Ken Research in their latest publication “India Pigments Market Outlook to 2022 – By Organic Pigments (Azo Pigments – Yellow, Red, Blue and Orange; Phthalocyanine – Green and Blue and HPP – Red, Orange and Yellow) and Inorganic Pigments (Titanium Oxide, Iron Oxide, Chrome Oxide and Others) and CPC Blue Crude Market” believe that focusing on specialty and high performance pigments, adopting for backward integration model to expand business operations, investing towards reducing adverse environmental effect, expansions through mergers and acquisitions, extending product/business portfolio, focusing towards eco-friendly/organic pigments and rising opportunities for non-toxic inorganic pigments will create a positive impact on the Indian pigments industry.

India market is expected to register a positive CAGR of 5.5% for pigments market during the forecast period 2017-2022E. Changes taking place in Chinese chemical industry has also presented several opportunities for Indian manufacturers to increase their exports, especially pigment emulsions towards major countries including US, Bangladesh, Germany, Turkey, China, Brazil, Italy and others.

Key Topics Covered in the report

India Phthalocyanine Pigment Market

Pricing Analysis India Pigments

Global Pigments Sales

Global Pigments Market

India Pigments Industry

Pigment Exports from India

Global Organic Pigment Forecast

Major Players in Pigments Industry

India Pigments Trends

Pigment Imports to India

Type of Pigments Sold in India

Major Selling Pigments in India

Inorganic Pigments Market India

Pigments Market Growth in India

Overall Chemicals Market in India

Export Sales Organic Pigment India

High Performance Pigments and Specialty Pigments Market

Companies Covered

Clariant Chemicals

Meghmani Organics

Sudarshan Chemicals

Asahi Songwon

Poddar Pigments

Kesar Petro products

Mazda Colors

Mallak Pigments

Pidilite Industries Limited

Phthalo Colors and Chemicals

Lona Industries

Gharda Chemicals Limited

Vibfast Pigments Pvt. Ltd.

For More Information, Refer to the Link below

Related Reports:

Contact Us:

Ken Research

Ankur Gupta, Head Marketing & Communications

+91-9015378249