What is the Potential of Indonesia

Healthcare Market?

The

Indonesia

Healthcare Market has shown a positive incline during 2012-2017 but

with respect to the expanding population of Indonesia, the market is still

underserved especially in the underdeveloped and rural areas as of 2017. People

across Indonesia are facing several health care issues due to sedentary

lifestyle and fast food consumption habits, such as obesity, diabetes, and

other cardiovascular diseases, which are demanding for technologically advanced

healthcare infrastructure. The healthcare market has increased on the account

of increasing healthcare facilities, innovation in pharmaceutical manufacturers

and clinical laboratory services and expansion of pharmacy retail chains across

the country. The market has witnessed enhancing innovation in nutritional

health segment, biopharmaceuticals and specialty pharmaceutical products.

Hospitals

in the country contributed to the maximum share of overall healthcare market as

of 2016. Over ~% of the market revenues were generated from the hospitals

segment followed by the pharmaceutical market with ~% in 2017.

The

Indonesia Healthcare market revenue has increased from USD ~ billion in 2012 to

USD ~ billion in 2017 primarily due to rising prevalence of non-communicable and

lifestyle diseases including diabetes, asthma and heart disorders. The industry

has undergone various deregulation programs which has encouraged foreign

investment in the industry. Furthermore, increase in demand for generic

medicines has led the major players in the industry to expand their production

capabilities.

How Has the JKN Scheme Impacted the

Indonesia Pharmaceutical Market?

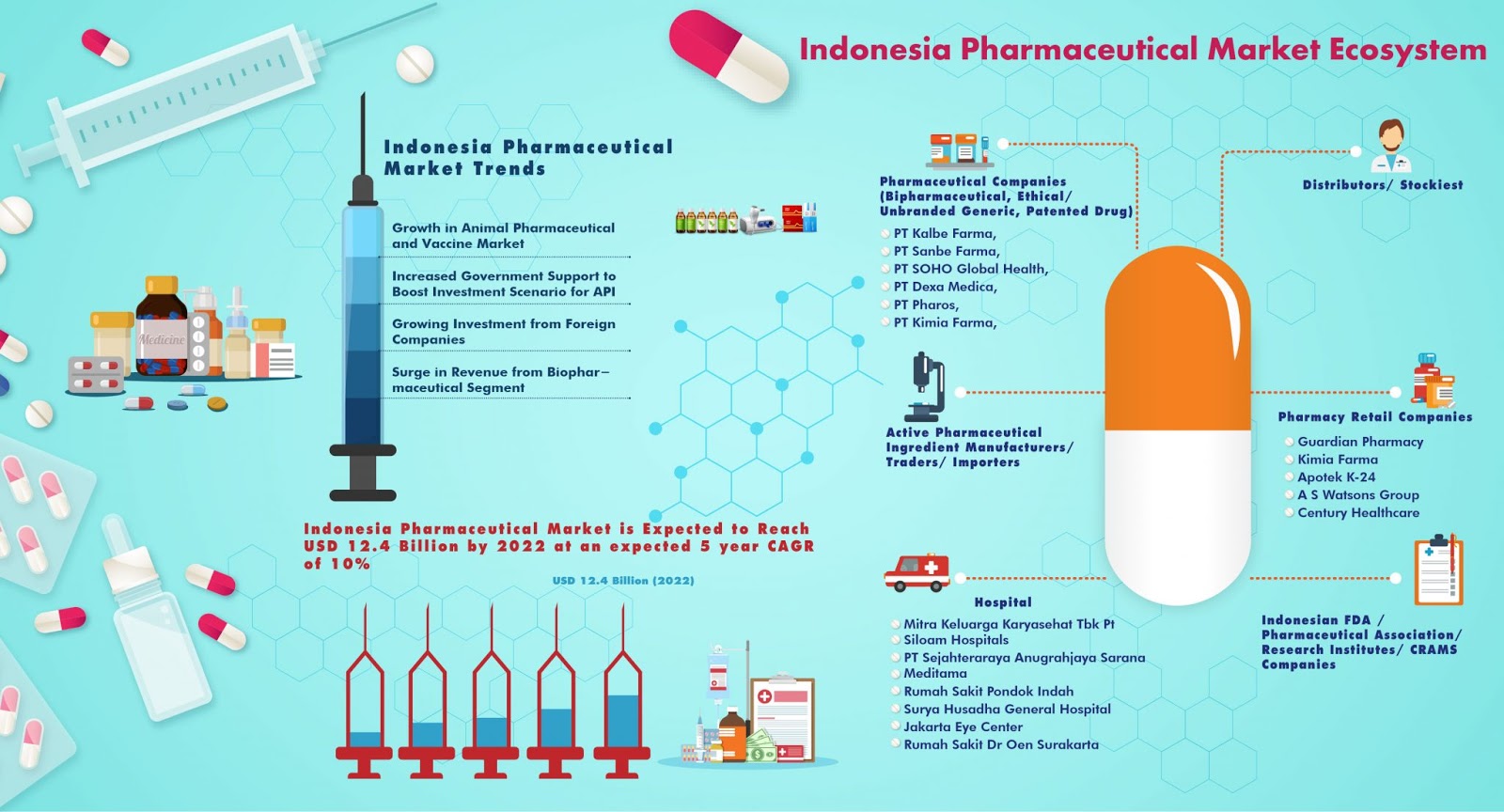

The

market size of Indonesia pharmaceutical industry has increased from USD ~

million in 2012 to USD ~ million in 2017 at a CAGR of ~%. The market is in the

growing stage supported by favorable government regulations and entry of

foreign players in the space. During 2017, the domestic players dominate the

market with major focus on production of generic drugs. This is driven by the

implementation of universal healthcare system. The program has led to an

increased demand for generic medicines from public and private hospitals

participating in the program. Further, the industry witnessed various

deregulation programs which encouraged foreign investment in the industry. For

instance, the government removed the pharmaceutical industry from its negative

investment list implying 100% foreign ownership is allowed. Major therapeutic

segments was anti-infective due to the prevalence of communicable diseases such

as TB, influenza and others followed by Gastrointestinal, cardiovascular,

Central nervous system, respiratory, musculoskeletal and dermatology.

How Have the Various Segments

Performed in Indonesia Pharmaceutical Market?

Anti-infective

drug sale has contributed to the largest share of ~% in the revenue share of

Indonesia Pharmaceutical industry in 2017. This is mainly due to high

prevalence of bacterial and communicable diseases. This is followed by

Gastrointestinal and metabolism drugs with ~%, cardiovascular system drugs with

~%, Central Nervous system drugs with ~%, and Respiratory system drugs with ~%.

The domestic players have accounted for ~% of the revenue in Indonesia

pharmaceutical market. International players have captured ~% of the revenue

share in 2017 driven by favorable government regulation. Generic drugs have

accounted for the major share of ~% of the revenue share in 2017. The share of

patented drugs has increased from ~% in 2013 to ~% in 2017.

How is the Competitive Ladscape of

Indonesia Pharmaceutical Market?

There

are ~ pharmaceutical companies (~ domestic and ~ international companies)

located in Indonesia and ~% of them are located in Java in 2016. These players

compete on the basis of distribution network, product portfolio, marketing

activities and research and development. The domestic players dominate the

generic drug and OTC drug segment.

How is the Indonesia Pharmacy Retail

Market Growing?

Indonesia

pharmacy retail sector is in the mid to late growth stage with the presence of

over ~ drugstores and pharmacies along with revenue CAGR of ~% in the last five

years. Already established players such Guardian Pharmacy, Kimia Farma, Apotek

K-24 have increased their number of pharmacy retail outlets over the period 2012-2017.

The number of pharmacies operated by Guardian pharmacy increased from ~ in 2013

to ~ in 2016 whereas for Kimia Farma, the number of pharmacies increased from ~

in 2013 to ~ in 2016. Over 2012-2017, the number of pharmacies has inclined at

a CAGR of ~%. Increasing incidence of life-style related ailments such as

Diabetes, Obesity, hypertension and various heart related diseases and

prevalence of communicable diseases such as TB, influenza among the growing

population are the main reasons behind positive growth in pharmacy retail

revenue due to growth in private label goods.

How Have the Various Segments

Performed in Indonesia Pharmacy Retail Market?

Pharmacies

have accounted for ~% of the share of Indonesia pharmacy retail revenue in 2017

whereas drugstores have accounted for ~% of the revenue share. The number of

pharmacies increased from ~ in 2012 to ~ in 2017 with average revenue of a

pharmacy estimated at IDR ~billion in 2017. The number of drugstores increased

from ~ in 2012 to ~ in 2017. West Java has gathered ~% of the total pharmacies

and drugstores in Indonesia in 2015. This can be attributed to more number of

hospitals located in the region. East Java has captured ~% of the pharmacies

and drugstores driven by increase in foreign investment in the pharmacy sector.

What are the Major Companies Operating

in This Space?

The

pharmacy retail market in Indonesia is highly fragmented with major organized

chains (Guardian pharmacy, Kimia Farma, Apotek K-24 and AS Watsons Group)

accounting for ~% of the revenue share in 2016. These players compete on

parameters such as proximity, value added services, availability of drugs,

promotional offers and tie ups with major healthcare institutions. In order to

increase their revenue, the players offer their products through online

portals.

What Factors have driven Indonesia

Clinical Laboratory Market?

Indonesia

Clinical Laboratory Market is in the growing stage. The market has grown at a

CAGR of ~% during 2012 to 2017 with revenue estimated at USD ~ billion in 2017.

The industry has witnessed expansion of private laboratory chains and use of

advanced technology in order to provide high quality laboratory services. With

the implementation of JKN, the demand for laboratory services has further

increased. The public hospitals mostly perform routine test while the esoteric

tests are outsourced to the private clinical laboratories. Due to growing awareness amongst people about

healthy living, private and public laboratories have witnessed an increase in

walk in patients asking for routine checkups which is funded out of the

patient’s pocket. Further, the major private laboratory chains have expanded

their operations in terms of capacity and geographic presence. The six major

private laboratories occupying ~% of the revenue share of Indonesia Private

independent labs in 2016 are Prodia, Kimia Farma, Pramita, Cito, Parahita and

BioMedika.

What are the Major Market Segments in

Indonesia Clinical Laboratory Market?

The

public clinical labs have accounted for ~% of the revenue share in Indonesia

clinical laboratory market in 2017. Private hospital labs have accounted for ~%

in 2017 and private independent labs with ~% of the overall market. The

laboratory chains have been the leading market players in Indonesia in 2016

with ~% of revenue in the overall private independent laboratory market in

2016. Single independent labs have contributed to their lower revenue share of

~% due to their restricted geographic presence.

What Are the Major Competition

Parameters?

The

private independent clinical laboratory market is organized and is composed of

both chain laboratories and stand-alone laboratories. The chain laboratories

are the leading market players in Indonesia. The 6 major players in the

industry are Prodia, Kimia Farma, Pramita, Cito, BioMedika and Parahita which

together accounted for ~% of the revenue share in private independent

laboratory market in 2017.

How has Indonesia Medical Device

Market Grown?

The

market was in the growing stage during 2012-2017 and is almost entirely import

driven. The market has seen increasing number of foreign players supported by

growing number of hospitals or other health centers in Indonesia. There were ~

medical device distributors and ~ medical device production units in Indonesia

as of 2015. Indonesian export performance for medical equipment commodity also

exhibited a positive trend. The main export destination for Indonesian medical

equipment are Singapore, Germany, Japan, the United States, China, the

Netherlands, India, Malaysia, Myanmar and Afghanistan. The demand has increased

majorly for diagnostic imaging, medical consumables, aesthetic, orthopedic and

dental products. This is driven by increased healthcare spending and rising

awareness about different treatment methods. Rising share of esoteric tests has

created demand for modern equipment such as pacemakers with micro-chip

technology, laser surgical device and test kits, which may include monoclonal

antibody technology.

How have the Different Segments in

Indonesia Medical Device Market Performed?

Diagnostic

imaging products have accounted for the largest share of ~% of the revenue

share in Indonesia Medical Devices market in 2017. This is followed by medical

consumable product with ~%, aesthetic devices with ~%, auxiliary devices with

~%, dental products with ~% and orthopedic implants with ~%. Hospitals both

public and private are the major end users of medical devices and have

accounted for ~% of the revenue in Indonesia Medical devices market in 2017.

The medical clinics and Laboratories and other healthcare institutions together

have contributed ~% of the revenue.

What are the Major Companies Operating

in the Space?

The

major local manufacturers include Indo Health Medical, PT Andini Sarana, PT

Trimitra Garmedindo Interbuana, PT Mega Andalan Kalasan and Citra Medika

Lestari. The major international players include GE Healthcare, Siemens,

Philips, Samsung and Hitachi. Major distributors include PT Mensa Bina Sukses,

PT Transmedic Indonesia and PT Surgika Alkesindo.

How has Indonesia Hospital Market

Grown?

The

hospital market grew at a five year CAGR of ~% during 2012-2017 from USD ~

billion in 2012 to USD ~ billion in 2017. Major driving factor for increase in

hospital market was the prevalence of the severe chronic diseases in Indonesia.

Several diseases like Pneumonia, Multi-bacillary (MB) Leprosy and Diarrhea had

increased in the year 2015. The number of specialty hospitals increased from ~

in 2012 to ~ in 2017. The industry is still in the nascent stage with huge scope

for development. The market has witnessed rise in use of digital healthcare

services. For instance, Practo entered the Indonesian market in 2015 providing

consumers the option of searching for doctors through a database of over 4,200

doctors, and covering 60% of the clinics in Jakarta DKI. Further, the market

revenue growth was facilitated by increase in the allocation of the Government

budget from IDR ~ Trillion in 2012 to IDR ~ Trillion in 2017. The foreign

investments rose from USD ~ million in the year 2015 to USD ~ million in the

year 2016.

How have the Major Segments in

Indonesia Hospital Market Performed?

Public

hospitals have accounted for ~% of the number of hospitals. Private hospitals

have registered ~% of the total hospitals in Indonesia in 2016 as the demand

for modern medicine and specialist services increased in the country. General

hospitals have accounted for ~% of the total number of hospitals whereas

specialty hospitals which include hospitals such as mental hospital, leprosy

hospital, eye hospital and others have registered ~% of the total number of

hospitals. Mother and children has accounted for ~% of the number of specialty

hospitals in 2015 followed by maternity hospitals with ~% and mental hospital

with ~% of the share in 2015. Rest of the market includes Eye hospital, leprosy

hospital and pulmonary tuberculosis hospital with ~%, ~% and ~% respectively of

the total number of specialty hospitals in 2015. East Java has gathered ~% of

the number of beds in Indonesia in 2016

Major

hospitals include Siloam Hospital group, Hermina Hospital Group, Rumah Sakit

Mitra, Awal Bros Hospital Group, Sari Asih Group, Ramsay Sime Darby Healthcare

and Eka Hospital group. Major competition parameters for private hospitals are

facilities, number of beds, number of hospitals, fees, quality of

doctors/medical practioners and specialization

For more information on the research

report, refer to below link:

Related Reports by Ken Research

Contact:

Ken

Research

Ankur

Gupta, Head Marketing & Communications

+91-124-4230204